Reversal with Bollinger Bands + RSI + ADX + ATR (Upgraded)Hi,

Welcome to my 4th script.

Someone asked me some questions about the Bollinger Band strategy I previously published. When I went back to my published script I couldn't help myself but simply try and make it better. Which I did.

Since I've published that script, I've gained much more knowledge about how Pinescript functions. As well as gaining more and more knowledge about how the markets are structered etc.

In this reversal script we use 4 indicators to determine good entry signals, we determine whether the market is ranging or trending and we still only want to take trades in the direction of the "trend".

Bollinger Bands are used for our entry signal. When price hits either side of the band, we wait for a reverse candlestick before we enter a position.

RSI is used to determine if we're in a trending market or in a ranging market. You can adjust the values in the inputs. You can determine the minimum RSI value and the maximum RSI value.

ADX is used the same way as RSI, you can adjust the value in the inputs. You can determine the minimum ADX value.

Last but not least we use two EMA's, a 200 EMA and 100 EMA. Both are adjustable through the inputs. I used two EMA's because I noticed when using this strategy that we'd enter a new position often after having a bad trade. Using two EMA's might clean up some signals, in my case with EUR/USD on a 15m timeframe, it didn't clean up enough signals.

All the default values are pretty decent but might require some finetuning on a certain instrument. Don't overfit the strategy though, that'll only give you bad signals in the future.

Then we are off to our exit signals.

Initially I wanted to incorporate my previous Bollinger Band exit signals as well, but it was too much of a hassle to make the script work as intended so I left it out. If you want to use those exit signals, just find my other script.

When we're in a position and price crosses the opposite band, we wait for a reverse candlestick before we exit the position.

Additionally we want our losses to be as small as possible, so we use RSI to signal us when the market is, or starts to, trend against us. This is where you use the minimum and maximum exit values. So when RSI crosses over or under that value, it'll exit the position.

Furthermore, we use the ATR indicator to set our stop loss, which is pretty basic stuff. You can adjust the ATR multiplier in the inputs. Disabling "Use Trailing Stop?" is really inadvisable unless you know this script inside out as your only exit signals will be opposite Bollinger Band Cross and RSI overbought / oversold areas.

Search in scripts for "the script"

RSI on VWAP Upgraded strategyFirst of all, the idea of apply RSI to VWAP was inspired by XaviZ; at least, that where I first saw that.

I simply applied the idea and searched for apply this on lower timeframe (M15) to increase the number of positions and improve the profit factor.

The conditions to enter are the same :

long : enter on RSI crossover oversold level

short : enter on RSI crossunder oversell level

To close position, I found a little change to apply :

long : close position when RSI(VWAP) went in overbought zone and crossunder the overbought level OR after being at least x bars in the overbought zone (parameter is 28 by default) => when the first condition happens

short : close position when RSI(VWAP) went in oversold zone and crossover the oversold level OR after being at least x bars in the oversell zone (parameter is 28 by default) => when the first condition happens

With this change, I got better results specially on BTCUSDTPERP (M15) where I reach a 6.8 profit factor with 119 trades closed. Not BAD !

The defaults parameters are the best found for BTCUSDTPERP (M15), but the strategy works fine for other pairs if you take time to find the rights combinations.

In this strategy you can change (with defaults in () ):

RSI length (28)

RSI overbought level (85)

RSI oversell level (30)

Number of bars before leaving as explain above (28)

The choice to take longs only, shorts only or both

The number of coin/token by position

The start date for backtesting

Please note that the script use a pyramiding parameter of 3 (can be changed in the first line of the script); that means that you can take up to 3 positions before closing. It lets you improve average enter price but increase the risk. 3 is the best I found to improve profit factor without expose myself too much.

This script would be better if automated because of the conditions of buy and sell.

It's only for educative purpose, not an advice to invest.

All my free scripts here : fr.tradingview.com

Leave a message and don't forget to follow me ;) !

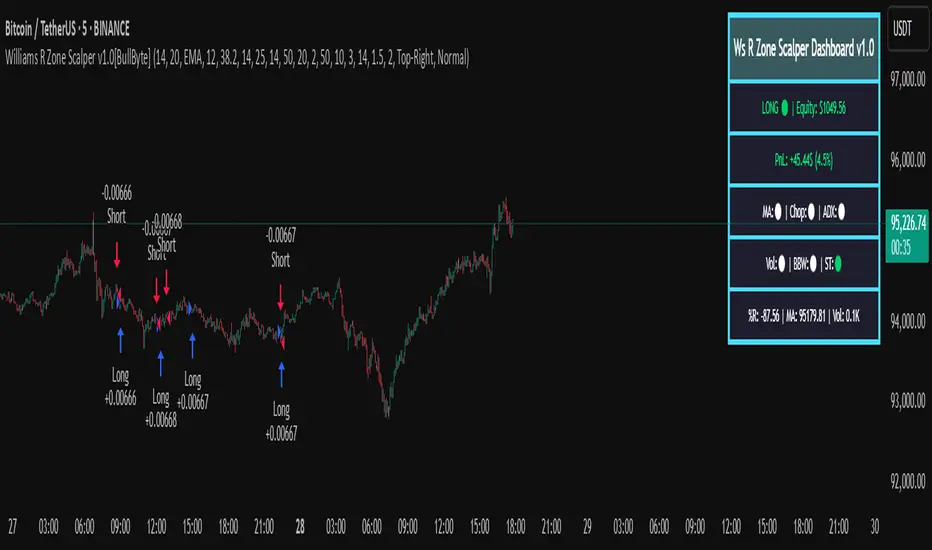

Williams R Zone Scalper v1.0[BullByte]Originality & Usefulness

Unlike standard Williams R cross-over scripts, this strategy layers five dynamic filters—moving-average trend, Supertrend, Choppiness Index, Bollinger Band Width, and volume validation —and presents a real-time dashboard with equity, PnL, filter status, and key indicator values. No other public Pine script combines these elements with toggleable filters and a custom dashboard. In backtests (BTC/USD (Binance), 5 min, 24 Mar 2025 → 28 Apr 2025), adding these filters turned a –2.09 % standalone Williams R into a +5.05 % net winner while cutting maximum drawdown in half.

---

What This Script Does

- Monitors Williams R (length 14) for overbought/oversold reversals.

- Applies up to five dynamic filters to confirm trend strength and volatility direction:

- Moving average (SMA/EMA/WMA/HMA)

- Supertrend line

- Choppiness Index (CI)

- Bollinger Band Width (BBW)

- Volume vs. its 50-period MA

- Plots blue arrows for Long entries (R crosses above –80 + all filters green) and red arrows for Short entries (R crosses below –20 + all filters green).

- Optionally sets dynamic ATR-based stop-loss (1.5×ATR) and take-profit (2×ATR).

- Shows a dashboard box with current position, equity, PnL, filter status, and real-time Williams R / MA/volume values.

---

Backtest Summary (BTC/USD(Binance), 5 min, 24 Mar 2025 → 28 Apr 2025)

• Total P&L : +50.70 USD (+5.05 %)

• Max Drawdown : 31.93 USD (3.11 %)

• Total Trades : 198

• Win Rate : 55.05 % (109/89)

• Profit Factor : 1.288

• Commission : 0.01 % per trade

• Slippage : 0 ticks

Even in choppy March–April, this multi-filter approach nets +5 % with a robust risk profile, compared to –2.09 % and higher drawdown for Williams R alone.

---

Williams R Alone vs. Multi-Filter Version

• Total P&L :

– Williams R alone → –20.83 USD (–2.09 %)

– Multi-Filter → +50.70 USD (+5.05 %)

• Max Drawdown :

– Williams R alone → 62.13 USD (6.00 %)

– Multi-Filter → 31.93 USD (3.11 %)

• Total Trades : 543 vs. 198

• Win Rate : 60.22 % vs. 55.05 %

• Profit Factor : 0.943 vs. 1.288

---

Inputs & What They Control

- wrLen (14): Williams R look-back

- maType (EMA): Trend filter type (SMA, EMA, WMA, HMA)

- maLen (20): Moving-average period

- useChop (true): Toggle Choppiness Index filter

- ciLen (12): CI look-back length

- chopThr (38.2): CI threshold (below = trending)

- useVol (true): Toggle volume-above-average filter

- volMaLen (50): Volume MA period

- useBBW (false): Toggle Bollinger Band Width filter

- bbwMaLen (50): BBW MA period

- useST (false): Toggle Supertrend filter

- stAtrLen (10): Supertrend ATR length

- stFactor (3.0): Supertrend multiplier

- useSL (false): Toggle ATR-based SL/TP

- atrLen (14): ATR period for SL/TP

- slMult (1.5): SL = slMult × ATR

- tpMult (2.0): TP = tpMult × ATR

---

How to Read the Chart

- Blue arrow (Long): Williams R crosses above –80 + all enabled filters green

- Red arrow (Short) : Williams R crosses below –20 + all filters green

- Dashboard box:

- Top : position and equity

- Next : cumulative PnL in USD & %

- Middle : green/white dots for each filter (green=passing, white=disabled)

- Bottom : Williams R, MA, and volume current values

---

Usage Tips

- Add the script : Indicators → My Scripts → Williams R Zone Scalper v1.0 → Add to BTC/USD chart on 5 min.

- Defaults : Optimized for BTC/USD.

- Forex majors : Raise `chopThr` to ~42.

- Stocks/high-beta : Enable `useBBW`.

- Enable SL/TP : Toggle `useSL`; stop-loss = 1.5×ATR, take-profit = 2×ATR apply automatically.

---

Common Questions

- * Why not trade every Williams R reversal?*

Raw Williams R whipsaws in sideways markets. Choppiness and volume filters reduce false entries.

- *Can I use on 1 min or 15 min?*

Yes—adjust ATR length or thresholds accordingly. Defaults target 5 min scalping.

- *What if all filters are on?*

Fewer arrows, higher-quality signals. Expect ~10 % boost in average win size.

---

Disclaimer & License

Trading carries risk of loss. Use this script “as is” under the Mozilla Public License 2.0 (mozilla.org). Always backtest, paper-trade, and adjust risk settings to your own profile.

---

Credits & References

- Pine Script v6, using TradingView’s built-in `ta.supertrend()`.

- TradingView House Rules: www.tradingview.com

Goodluck!

BullByte

Só Trade Top - Média de 8 - Augusto BackesThis strategy is an ADAPTATION of the EMA8 Setup from Augusto Backes (brazilian crypto youtuber).

The strategy was designed to work on the daily timeframe with the weekly EMA8.

Buy signals when there is a bullish candle above the weekly EMA8 - bullish candles in the script: engulfing candles, closing price reversal and bullish hammer.

Exit signals when there is a bearish candle below the weekly EMA8 - bearish candles in script: engulfing candles, closing price reversal and bearish hammer.

Entries and Exits on signals close.

Risk Management: all in on every trade.

The results here shown are from the standard parameters of the strategy.

------------------------------------------------------------------------------------------------------

PORTUGUESE TRANSLATION

------------------------------------------------------------------------------------------------------

Essa estratégia é uma adaptação do setup EMA8 do youtuber crypto Augusto Backes.

A estratégia foi desenvolvida para trabalhar em gráficos diários, usando a EMA8 do gráfico semanal.

Sinais de compra: quando uma figura de alta acontece acima da EMA8 semanal. Figuras de alta consideradas: Engolfo de Alta, Preço de fechamento de reversão de alta e Martelo de Alta

Sinais de saída do trade: quando uma figura de baixa acontece abaixo da EMA8 semanal. Figuras de baixa consideradas: Engolfo de Baixa, Preço de fechamento de reversão de baixa e Martelo de Baixa.

Todas as ordens são executadas dos fechamentos dos candles de sinal.

Gestão de risco: 100% do capital em cada trade.

Os resultados mostrados são com a aplicação dos parâmetros padrão da estratégia.

Kernel Regression Envelope with SMI OscillatorThis script combines the predictive capabilities of the **Nadaraya-Watson estimator**, implemented by the esteemed jdehorty (credit to him for his excellent work on the `KernelFunctions` library and the original Nadaraya-Watson Envelope indicator), with the confirmation strength of the **Stochastic Momentum Index (SMI)** to create a dynamic trend reversal strategy. The core idea is to identify potential overbought and oversold conditions using the Nadaraya-Watson Envelope and then confirm these signals with the SMI before entering a trade.

**Understanding the Nadaraya-Watson Envelope:**

The Nadaraya-Watson estimator is a non-parametric regression technique that essentially calculates a weighted average of past price data to estimate the current underlying trend. Unlike simple moving averages that give equal weight to all past data within a defined period, the Nadaraya-Watson estimator uses a **kernel function** (in this case, the Rational Quadratic Kernel) to assign weights. The key parameters influencing this estimation are:

* **Lookback Window (h):** This determines how many historical bars are considered for the estimation. A larger window results in a smoother estimation, while a smaller window makes it more reactive to recent price changes.

* **Relative Weighting (alpha):** This parameter controls the influence of different time frames in the estimation. Lower values emphasize longer-term price action, while higher values make the estimator more sensitive to shorter-term movements.

* **Start Regression at Bar (x\_0):** This allows you to exclude the potentially volatile initial bars of a chart from the calculation, leading to a more stable estimation.

The script calculates the Nadaraya-Watson estimation for the closing price (`yhat_close`), as well as the highs (`yhat_high`) and lows (`yhat_low`). The `yhat_close` is then used as the central trend line.

**Dynamic Envelope Bands with ATR:**

To identify potential entry and exit points around the Nadaraya-Watson estimation, the script uses **Average True Range (ATR)** to create dynamic envelope bands. ATR measures the volatility of the price. By multiplying the ATR by different factors (`nearFactor` and `farFactor`), we create multiple bands:

* **Near Bands:** These are closer to the Nadaraya-Watson estimation and are intended to identify potential immediate overbought or oversold zones.

* **Far Bands:** These are further away and can act as potential take-profit or stop-loss levels, representing more extreme price extensions.

The script calculates both near and far upper and lower bands, as well as an average between the near and far bands. This provides a nuanced view of potential support and resistance levels around the estimated trend.

**Confirming Reversals with the Stochastic Momentum Index (SMI):**

While the Nadaraya-Watson Envelope identifies potential overextended conditions, the **Stochastic Momentum Index (SMI)** is used to confirm a potential trend reversal. The SMI, unlike a traditional stochastic oscillator, oscillates around a zero line. It measures the location of the current closing price relative to the median of the high/low range over a specified period.

The script calculates the SMI on a **higher timeframe** (defined by the "Timeframe" input) to gain a broader perspective on the market momentum. This helps to filter out potential whipsaws and false signals that might occur on the current chart's timeframe. The SMI calculation involves:

* **%K Length:** The lookback period for calculating the highest high and lowest low.

* **%D Length:** The period for smoothing the relative range.

* **EMA Length:** The period for smoothing the SMI itself.

The script uses a double EMA for smoothing within the SMI calculation for added smoothness.

**How the Indicators Work Together in the Strategy:**

The strategy enters a long position when:

1. The closing price crosses below the **near lower band** of the Nadaraya-Watson Envelope, suggesting a potential oversold condition.

2. The SMI crosses above its EMA, indicating positive momentum.

3. The SMI value is below -50, further supporting the oversold idea on the higher timeframe.

Conversely, the strategy enters a short position when:

1. The closing price crosses above the **near upper band** of the Nadaraya-Watson Envelope, suggesting a potential overbought condition.

2. The SMI crosses below its EMA, indicating negative momentum.

3. The SMI value is above 50, further supporting the overbought idea on the higher timeframe.

Trades are closed when the price crosses the **far band** in the opposite direction of the trade. A stop-loss is also implemented based on a fixed value.

**In essence:** The Nadaraya-Watson Envelope identifies areas where the price might be deviating significantly from its estimated trend. The SMI, calculated on a higher timeframe, then acts as a confirmation signal, suggesting that the momentum is shifting in the direction of a potential reversal. The ATR-based bands provide dynamic entry and exit points based on the current volatility.

**How to Use the Script:**

1. **Apply the script to your chart.**

2. **Adjust the "Kernel Settings":**

* **Lookback Window (h):** Experiment with different values to find the smoothness that best suits the asset and timeframe you are trading. Lower values make the envelope more reactive, while higher values make it smoother.

* **Relative Weighting (alpha):** Adjust to control the influence of different timeframes on the Nadaraya-Watson estimation.

* **Start Regression at Bar (x\_0):** Increase this value if you want to exclude the initial, potentially volatile, bars from the calculation.

* **Stoploss:** Set your desired stop-loss value.

3. **Adjust the "SMI" settings:**

* **%K Length, %D Length, EMA Length:** These parameters control the sensitivity and smoothness of the SMI. Experiment to find settings that work well for your trading style.

* **Timeframe:** Select the higher timeframe you want to use for SMI confirmation.

4. **Adjust the "ATR Length" and "Near/Far ATR Factor":** These settings control the width and sensitivity of the envelope bands. Smaller ATR lengths make the bands more reactive to recent volatility.

5. **Customize the "Color Settings"** to your preference.

6. **Observe the plots:**

* The **Nadaraya-Watson Estimation (yhat)** line represents the estimated underlying trend.

* The **near and far upper and lower bands** visualize potential overbought and oversold zones based on the ATR.

* The **fill areas** highlight the regions between the near and far bands.

7. **Look for entry signals:** A long entry is considered when the price touches or crosses below the lower near band and the SMI confirms upward momentum. A short entry is considered when the price touches or crosses above the upper near band and the SMI confirms downward momentum.

8. **Manage your trades:** The script provides exit signals when the price crosses the far band. The fixed stop-loss will also close trades if the price moves against your position.

**Justification for Combining Nadaraya-Watson Envelope and SMI:**

The combination of the Nadaraya-Watson Envelope and the SMI provides a more robust approach to identifying potential trend reversals compared to using either indicator in isolation. The Nadaraya-Watson Envelope excels at identifying potential areas where the price is overextended relative to its recent history. However, relying solely on the envelope can lead to false signals, especially in choppy or volatile markets. By incorporating the SMI as a confirmation tool, we add a momentum filter that helps to validate the potential reversals signaled by the envelope. The higher timeframe SMI further helps to filter out noise and focus on more significant shifts in momentum. The ATR-based bands add a dynamic element to the entry and exit points, adapting to the current market volatility. This mashup aims to leverage the strengths of each indicator to create a more reliable trading strategy.

Table to filter trades per dayThis script contains a block of code that allows users to filter the total number of trades, loss trades, win trades and win rate per day in a table. This makes it easier to compare which days were profitable and which were not.

Be aware that this script can only be used in strategy scripts. To use the script, open it and copy every line from "START" to "STOP". Then, paste these lines at the very bottom of the strategy script that you want to attach it to.

The user has the ability to adjust the position of the table and customize the size of the text displayed.

If the user sets "Check when the trade:" to "Opened", the script will monitor when the trade opens and add it to the table once it has been closed. If "Check when the trade:" is set to "Closed", the script will track when the trade is closed and add it to the table once it has been closed.

It is recommended to run the script on the "Exchange" setting for more accurate results, even though a "Set the timezone" option is available. This will prevent discrepancies caused by daylight saving time changes.

Please note that the code will only work properly if you choose a daily timeframe or lower.

JS-TechTrading: VWAP Momentum_Pullback StrategyGeneral Description and Unique Features of this Script

Introducing the VWAP Momentum-Pullback Strategy (long-only) that offers several unique features:

1. Our script/strategy utilizes Mark Minervini's Trend-Template as a qualifier for identifying stocks and other financial securities in confirmed uptrends.

NOTE: In this basic version of the script, the Trend-Template has to be used as a separate indicator on TradingView (Public Trend-Template indicators are available on TradingView – community scripts). It is recommended to only execute buy signals in case the stock or financial security is in a stage 2 uptrend, which means that the criteria of the trend-template are fulfilled.

2. Our strategy is based on the supply/demand balance in the market, making it timeless and effective across all timeframes. Whether you are day trading using 1- or 5-min charts or swing-trading using daily charts, this strategy can be applied and works very well.

3. We have also integrated technical indicators such as the RSI and the MA / VWAP crossover into this strategy to identify low-risk pullback entries in the context of confirmed uptrends. By doing so, the risk profile of this strategy and drawdowns are being reduced to an absolute minimum.

Minervini’s Trend-Template and the ‘Stage-Analysis’ of the Markets

This strategy is a so-called 'long-only' strategy. This means that we only take long positions, short positions are not considered.

The best market environment for such strategies are periods of stable upward trends in the so-called stage 2 - uptrend.

In stable upward trends, we increase our market exposure and risk.

In sideways markets and downward trends or bear markets, we reduce our exposure very quickly or go 100% to cash and wait for the markets to recover and improve. This allows us to avoid major losses and drawdowns.

This simple rule gives us a significant advantage over most undisciplined traders and amateurs!

'The Trend is your Friend'. This is a very old but true quote.

What's behind it???

• 98% of stocks made their biggest gains in a Phase 2 upward trend.

• If a stock is in a stable uptrend, this is evidence that larger institutions are buying the stock sustainably.

• By focusing on stocks that are in a stable uptrend, the chances of profit are significantly increased.

• In a stable uptrend, investors know exactly what to expect from further price developments. This makes it possible to locate low-risk entry points.

The goal is not to buy at the lowest price – the goal is to buy at the right price!

Each stock goes through the same maturity cycle – it starts at stage 1 and ends at stage 4

Stage 1 – Neglect Phase – Consolidation

Stage 2 – Progressive Phase – Accumulation

Stage 3 – Topping Phase – Distribution

Stage 4 – Downtrend – Capitulation

This strategy focuses on identifying stocks in confirmed stage 2 uptrends. This in itself gives us an advantage over long-term investors and less professional traders.

By focusing on stocks in a stage 2 uptrend, we avoid losses in downtrends (stage 4) or less profitable consolidation phases (stages 1 and 3). We are fully invested and put our money to work for us, and we are fully invested when stocks are in their stage 2 uptrends.

But how can we use technical chart analysis to find stocks that are in a stable stage 2 uptrend?

Mark Minervini has developed the so-called 'trend template' for this purpose. This is an essential part of our JS-TechTrading pullback strategy. For our watchlists, only those individual values that meet the tough requirements of Minervini's trend template are eligible.

The Trend Template

• 200d MA increasing over a period of at least 1 month, better 4-5 months or longer

• 150d MA above 200d MA

• 50d MA above 150d MA and 200d MA

• Course above 50d MA, 150d MA and 200d MA

• Ideally, the 50d MA is increasing over at least 1 month

• Price at least 25% above the 52w low

• Price within 25% of 52w high

• High relative strength according to IBD.

NOTE: In this basic version of the script, the Trend-Template has to be used as a separate indicator on TradingView (Public Trend-Template indicators are available in TradingView – community scripts). It is recommended to only execute buy signals in case the stock or financial security is in a stage 2 uptrend, which means that the criteria of the trend-template are fulfilled.

This strategy can be applied to all timeframes from 5 min to daily.

The VWAP Momentum-Pullback Strateg y

For the JS-TechTrading VWAP Momentum-Pullback Strategy, only stocks and other financial instruments that meet the selected criteria of Mark Minervini's trend template are recommended for algorithmic trading with this startegy.

A further prerequisite for generating a buy signals is that the individual value is in a short-term oversold state (RSI).

When the selling pressure is over and the continuation of the uptrend can be confirmed by the MA / VWAP crossover after reaching a price low, a buy signal is issued by this strategy.

Stop-loss limits and profit targets can be set variably.

Relative Strength Index (RSI)

The Relative Strength Index (RSI) is a technical indicator developed by Welles Wilder in 1978. The RSI is used to perform a market value analysis and identify the strength of a trend as well as overbought and oversold conditions. The indicator is calculated on a scale from 0 to 100 and shows how much an asset has risen or fallen relative to its own price in recent periods.

The RSI is calculated as the ratio of average profits to average losses over a certain period of time. A high value of the RSI indicates an overbought situation, while a low value indicates an oversold situation. Typically, a value > 70 is considered an overbought threshold and a value < 30 is considered an oversold threshold. A value above 70 signals that a single value may be overvalued and a decrease in price is likely , while a value below 30 signals that a single value may be undervalued and an increase in price is likely.

For example, let's say you're watching a stock XYZ. After a prolonged falling movement, the RSI value of this stock has fallen to 26. This means that the stock is oversold and that it is time for a potential recovery. Therefore, a trader might decide to buy this stock in the hope that it will rise again soon.

The MA / VWAP Crossover Trading Strategy

This strategy combines two popular technical indicators: the Moving Average (MA) and the Volume Weighted Average Price (VWAP). The MA VWAP crossover strategy is used to identify potential trend reversals and entry/exit points in the market.

The VWAP is calculated by taking the average price of an asset for a given period, weighted by the volume traded at each price level. The MA, on the other hand, is calculated by taking the average price of an asset over a specified number of periods. When the MA crosses above the VWAP, it suggests that buying pressure is increasing, and it may be a good time to enter a long position. When the MA crosses below the VWAP, it suggests that selling pressure is increasing, and it may be a good time to exit a long position or enter a short position.

Traders typically use the MA VWAP crossover strategy in conjunction with other technical indicators and fundamental analysis to make more informed trading decisions. As with any trading strategy, it is important to carefully consider the risks and potential rewards before making any trades.

This strategy is applicable to all timeframes and the relevant parameters for the underlying indicators (RSI and MA/VWAP) can be adjusted and optimized as needed.

Backtesting

Backtesting gives outstanding results on all timeframes and drawdowns can be reduced to a minimum level. In this example, the hourly chart for MCFT has been used.

Settings for backtesting are:

- Period from April 2020 until April 2021 (1 yr)

- Starting capital 100k USD

- Position size = 25% of equity

- 0.01% commission = USD 2.50.- per Trade

- Slippage = 2 ticks

Other comments

• This strategy has been designed to identify the most promising, highest probability entries and trades for each stock or other financial security.

• The RSI qualifier is highly selective and filters out the most promising swing-trading entries. As a result, you will normally only find a low number of trades for each stock or other financial security per year in case you apply this strategy for the daily charts. Shorter timeframes will result in a higher number of trades / year.

• As a result, traders need to apply this strategy for a full watchlist rather than just one financial security.

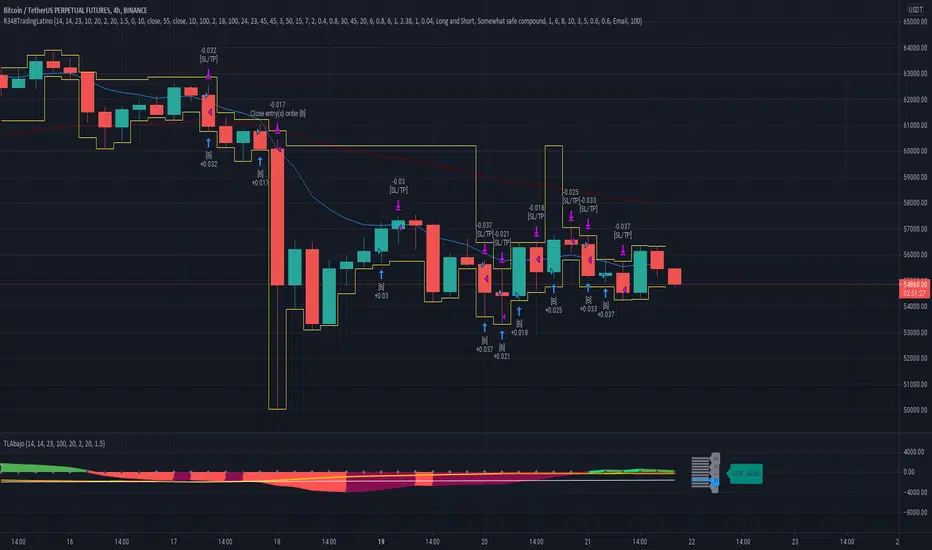

Ruckard TradingLatinoThis strategy tries to mimic TradingLatino strategy.

The current implementation is beta.

Si hablas castellano o espanyol por favor consulta MENSAJE EN CASTELLANO más abajo.

It's aimed at BTCUSDT pair and 4h timeframe.

STRATEGY DEFAULT SETTINGS EXPLANATION

max_bars_back=5000 : This is a random number of bars so that the strategy test lasts for one or two years

calc_on_order_fills=false : To wait for the 4h closing is too much. Try to check if it's worth entering a position after closing one. I finally decided not to recheck if it's worth entering after an order is closed. So it is false.

calc_on_every_tick=false

pyramiding=0 : We only want one entry allowed in the same direction. And we don't want the order to scale by error.

initial_capital=1000 : These are 1000 USDT. By using 1% maximum loss per trade and 7% as a default stop loss by using 1000 USDT at 12000 USDT per BTC price you would entry with around 142 USDT which are converted into: 0.010 BTC . The maximum number of decimal for contracts on this BTCUSDT market is 3 decimals. E.g. the minimum might be: 0.001 BTC . So, this minimal 1000 amount ensures us not to entry with less than 0.001 entries which might have happened when using 100 USDT as an initial capital.

slippage=1 : Binance BTCUSDT mintick is: 0.01. Binance slippage: 0.1 % (Let's assume). TV has an integer slippage. It does not have a percentage based slippage. If we assume a 1000 initial capital, the recommended equity is 142 which at 11996 USDT per BTC price means: 0.011 BTC. The 0.1% slippage of: 0.011 BTC would be: 0.000011 . This is way smaller than the mintick. So our slippage is going to be 1. E.g. 1 (slippage) * 0.01 (mintick)

commission_type=strategy.commission.percent and commission_value=0.1 : According to: binance . com / en / fee / schedule in VIP 0 level both maker and taker fees are: 0.1 %.

BACKGROUND

Jaime Merino is a well known Youtuber focused on crypto trading

His channel TradingLatino

features monday to friday videos where he explains his strategy.

JAIME MERINO STANCE ON BOTS

Jaime Merino stance on bots (taken from memory out of a 2020 June video from him):

'~

You know. They can program you a bot and it might work.

But, there are some special situations that the bot would not be able to handle.

And, I, as a human, I would handle it. And the bot wouldn't do it.

~'

My long term target with this strategy script is add as many

special situations as I can to the script

so that it can match Jaime Merino behaviour even in non normal circumstances.

My alternate target is learn Pine script

and enjoy programming with it.

WARNING

This script might be bigger than other TradingView scripts.

However, please, do not be confused because the current status is beta.

This script has not been tested with real money.

This is NOT an official strategy from Jaime Merino.

This is NOT an official strategy from TradingLatino . net .

HOW IT WORKS

It basically uses ADX slope and LazyBear's Squeeze Momentum Indicator

to make its buy and sell decisions.

Fast paced EMA being bigger than slow paced EMA

(on higher timeframe) advices going long.

Fast paced EMA being smaller than slow paced EMA

(on higher timeframe) advices going short.

It finally add many substrats that TradingLatino uses.

SETTINGS

__ SETTINGS - Basics

____ SETTINGS - Basics - ADX

(ADX) Smoothing {14}

(ADX) DI Length {14}

(ADX) key level {23}

____ SETTINGS - Basics - LazyBear Squeeze Momentum

(SQZMOM) BB Length {20}

(SQZMOM) BB MultFactor {2.0}

(SQZMOM) KC Length {20}

(SQZMOM) KC MultFactor {1.5}

(SQZMOM) Use TrueRange (KC) {True}

____ SETTINGS - Basics - EMAs

(EMAS) EMA10 - Length {10}

(EMAS) EMA10 - Source {close}

(EMAS) EMA55 - Length {55}

(EMAS) EMA55 - Source {close}

____ SETTINGS - Volume Profile

Lowest and highest VPoC from last three days

is used to know if an entry has a support

VPVR of last 100 4h bars

is also taken into account

(VP) Use number of bars (not VP timeframe): Uses 'Number of bars {100}' setting instead of 'Volume Profile timeframe' setting for calculating session VPoC

(VP) Show tick difference from current price {False}: BETA . Might be useful for actions some day.

(VP) Number of bars {100}: If 'Use number of bars (not VP timeframe)' is turned on this setting is used to calculate session VPoC.

(VP) Volume Profile timeframe {1 day}: If 'Use number of bars (not VP timeframe)' is turned off this setting is used to calculate session VPoC.

(VP) Row width multiplier {0.6}: Adjust how the extra Volume Profile bars are shown in the chart.

(VP) Resistances prices number of decimal digits : Round Volume Profile bars label numbers so that they don't have so many decimals.

(VP) Number of bars for bottom VPOC {18}: 18 bars equals 3 days in suggested timeframe of 4 hours. It's used to calculate lowest session VPoC from previous three days. It's also used as a top VPOC for sells.

(VP) Ignore VPOC bottom advice on long {False}: If turned on it ignores bottom VPOC (or top VPOC on sells) when evaluating if a buy entry is worth it.

(VP) Number of bars for VPVR VPOC {100}: Number of bars to calculate the VPVR VPoC. We use 100 as Jaime once used. When the price bounces back to the EMA55 it might just bounce to this VPVR VPoC if its price it's lower than the EMA55 (Sells have inverse algorithm).

____ SETTINGS - ADX Slope

ADX Slope

help us to understand if ADX

has a positive slope, negative slope

or it is rather still.

(ADXSLOPE) ADX cut {23}: If ADX value is greater than this cut (23) then ADX has strength

(ADXSLOPE) ADX minimum steepness entry {45}: ADX slope needs to be 45 degrees to be considered as a positive one.

(ADXSLOPE) ADX minimum steepness exit {45}: ADX slope needs to be -45 degrees to be considered as a negative one.

(ADXSLOPE) ADX steepness periods {3}: In order to avoid false detection the slope is calculated along 3 periods.

____ SETTINGS - Next to EMA55

(NEXTEMA55) EMA10 to EMA55 bounce back percentage {80}: EMA10 might bounce back to EMA55 or maybe to 80% of its complete way to EMA55

(NEXTEMA55) Next to EMA55 percentage {15}: How much next to the EMA55 you need to be to consider it's going to bounce back upwards again.

____ SETTINGS - Stop Loss and Take Profit

You can set a default stop loss or a default take profit.

(STOPTAKE) Stop Loss % {7.0}

(STOPTAKE) Take Profit % {2.0}

____ SETTINGS - Trailing Take Profit

You can customize the default trailing take profit values

(TRAILING) Trailing Take Profit (%) {1.0}: Trailing take profit offset in percentage

(TRAILING) Trailing Take Profit Trigger (%) {2.0}: When 2.0% of benefit is reached then activate the trailing take profit.

____ SETTINGS - MAIN TURN ON/OFF OPTIONS

(EMAS) Ignore advice based on emas {false}.

(EMAS) Ignore advice based on emas (On closing long signal) {False}: Ignore advice based on emas but only when deciding to close a buy entry.

(SQZMOM) Ignore advice based on SQZMOM {false}: Ignores advice based on SQZMOM indicator.

(ADXSLOPE) Ignore advice based on ADX positive slope {false}

(ADXSLOPE) Ignore advice based on ADX cut (23) {true}

(STOPTAKE) Take Profit? {false}: Enables simple Take Profit.

(STOPTAKE) Stop Loss? {True}: Enables simple Stop Loss.

(TRAILING) Enable Trailing Take Profit (%) {True}: Enables Trailing Take Profit.

____ SETTINGS - Strategy mode

(STRAT) Type Strategy: 'Long and Short', 'Long Only' or 'Short Only'. Default: 'Long and Short'.

____ SETTINGS - Risk Management

(RISKM) Risk Management Type: 'Safe', 'Somewhat safe compound' or 'Unsafe compound'. ' Safe ': Calculations are always done with the initial capital (1000) in mind. The maximum losses per trade/day/week/month are taken into account. ' Somewhat safe compound ': Calculations are done with initial capital (1000) or a higher capital if it increases. The maximum losses per trade/day/week/month are taken into account. ' Unsafe compound ': In each order all the current capital is gambled and only the default stop loss per order is taken into account. That means that the maximum losses per trade/day/week/month are not taken into account. Default : 'Somewhat safe compound'.

(RISKM) Maximum loss per trade % {1.0}.

(RISKM) Maximum loss per day % {6.0}.

(RISKM) Maximum loss per week % {8.0}.

(RISKM) Maximum loss per month % {10.0}.

____ SETTINGS - Decimals

(DECIMAL) Maximum number of decimal for contracts {3}: How small (3 decimals means 0.001) an entry position might be in your exchange.

EXTRA 1 - PRICE IS IN RANGE indicator

(PRANGE) Print price is in range {False}: Enable a bottom label that indicates if the price is in range or not.

(PRANGE) Price range periods {5}: How many previous periods are used to calculate the medians

(PRANGE) Price range maximum desviation (%) {0.6} ( > 0 ): Maximum positive desviation for range detection

(PRANGE) Price range minimum desviation (%) {0.6} ( > 0 ): Mininum negative desviation for range detection

EXTRA 2 - SQUEEZE MOMENTUM Desviation indicator

(SQZDIVER) Show degrees {False}: Show degrees of each Squeeze Momentum Divergence lines to the x-axis.

(SQZDIVER) Show desviation labels {False}: Whether to show or not desviation labels for the Squeeze Momentum Divergences.

(SQZDIVER) Show desviation lines {False}: Whether to show or not desviation lines for the Squeeze Momentum Divergences.

EXTRA 3 - VOLUME PROFILE indicator

WARNING: This indicator works not on current bar but on previous bar. So in the worst case it might be VP from 4 hours ago. Don't worry, inside the strategy calculus the correct values are used. It's just that I cannot show the most recent one in the chart.

(VP) Print recent profile {False}: Show Volume Profile indicator

(VP) Avoid label price overlaps {False}: Avoid label prices to overlap on the chart.

EXTRA 4 - ZIGNALY SUPPORT

(ZIG) Zignaly Alert Type {Email}: 'Email', 'Webhook'. ' Email ': Prepare alert_message variable content to be compatible with zignaly expected email content format. ' Webhook ': Prepare alert_message variable content to be compatible with zignaly expected json content format.

EXTRA 5 - DEBUG

(DEBUG) Enable debug on order comments {False}: If set to true it prepares the order message to match the alert_message variable. It makes easier to debug what would have been sent by email or webhook on each of the times an order is triggered.

HOW TO USE THIS STRATEGY

BOT MODE: This is the default setting.

PROPER VOLUME PROFILE VIEWING: Click on this strategy settings. Properties tab. Make sure Recalculate 'each time the order was run' is turned off.

NEWBIE USER: (Check PROPER VOLUME PROFILE VIEWING above!) You might want to turn on the 'Print recent profile {False}' setting. Alternatively you can use my alternate realtime study: 'Resistances and supports based on simplified Volume Profile' but, be aware, it might consume one indicator.

ADVANCED USER 1: Turn on the 'Print price is in range {False}' setting and help us to debug this subindicator. Also help us to figure out how to include this value in the strategy.

ADVANCED USER 2: Turn on the all the (SQZDIVER) settings and help us to figure out how to include this value in the strategy.

ADVANCED USER 3: (Check PROPER VOLUME PROFILE VIEWING above!) Turn on the 'Print recent profile {False}' setting and report any problem with it.

JAIME MERINO: Just use the indicator as it comes by default. It should only show BUY signals, SELL signals and their associated closing signals. From time to time you might want to check 'ADVANCED USER 2' instructions to check that there's actually a divergence. Check also 'ADVANCED USER 1' instructions for your amusement.

EXTRA ADVICE

It's advised that you use this strategy in addition to these two other indicators:

* Squeeze Momentum Indicator

* ADX

so that your chart matches as close as possible to TradingLatino chart.

ZIGNALY INTEGRATION

This strategy supports Zignaly email integration by default. It also supports Zignaly Webhook integration.

ZIGNALY INTEGRATION - Email integration example

What you would write in your alert message:

||{{strategy.order.alert_message}}||key=MYSECRETKEY||

ZIGNALY INTEGRATION - Webhook integration example

What you would write in your alert message:

{ {{strategy.order.alert_message}} , "key" : "MYSECRETKEY" }

CREDITS

I have reused and adapted some code from

'Directional Movement Index + ADX & Keylevel Support' study

which it's from TradingView console user.

I have reused and adapted some code from

'3ema' study

which it's from TradingView hunganhnguyen1193 user.

I have reused and adapted some code from

'Squeeze Momentum Indicator ' study

which it's from TradingView LazyBear user.

I have reused and adapted some code from

'Strategy Tester EMA-SMA-RSI-MACD' study

which it's from TradingView fikira user.

I have reused and adapted some code from

'Support Resistance MTF' study

which it's from TradingView LonesomeTheBlue user.

I have reused and adapted some code from

'TF Segmented Linear Regression' study

which it's from TradingView alexgrover user.

I have reused and adapted some code from

"Poor man's volume profile" study

which it's from TradingView IldarAkhmetgaleev user.

FEEDBACK

Please check the strategy source code for more detailed information

where, among others, I explain all of the substrats

and if they are implemented or not.

Q1. Did I understand wrong any of the Jaime substrats (which I have implemented)?

Q2. The strategy yields quite profit when we should long (EMA10 from 1d timeframe is higher than EMA55 from 1d timeframe.

Why the strategy yields much less profit when we should short (EMA10 from 1d timeframe is lower than EMA55 from 1d timeframe)?

Any idea if you need to do something else rather than just reverse what Jaime does when longing?

FREQUENTLY ASKED QUESTIONS

FAQ1. Why are you giving this strategy for free?

TradingLatino and his fellow enthusiasts taught me this strategy. Now I'm giving back to them.

FAQ2. Seriously! Why are you giving this strategy for free?

I'm confident his strategy might be improved a lot. By keeping it to myself I would avoid other people contributions to improve it.

Now that everyone can contribute this is a win-win.

FAQ3. How can I connect this strategy to my Exchange account?

It seems that you can attach alerts to strategies.

You might want to combine it with a paying account which enable Webhook URLs to work.

I don't know how all of this works right now so I cannot give you advice on it.

You will have to do your own research on this subject. But, be careful. Automating trades, if not done properly,

might end on you automating losses.

FAQ4. I have just found that this strategy by default gives more than 3.97% of 'maximum series of losses'. That's unacceptable according to my risk management policy.

You might want to reduce default stop loss setting from 7% to something like 5% till you are ok with the 'maximum series of losses'.

FAQ5. Where can I learn more about your work on this strategy?

Check the source code. You might find unused strategies. Either because there's not a substantial increases on earnings. Or maybe because they have not been implemented yet.

FAQ6. How much leverage is applied in this strategy?

No leverage.

FAQ7. Any difference with original Jaime Merino strategy?

Most of the times Jaime defines an stop loss at the price entry. That's not the case here. The default stop loss is 7% (but, don't be confused it only means losing 1% of your investment thanks to risk management). There's also a trailing take profit that triggers at 2% profit with a 1% trailing.

FAQ8. Why this strategy return is so small?

The strategy should be improved a lot. And, well, backtesting in this platform is not guaranteed to return theoric results comparable to real-life returns. That's why I'm personally forward testing this strategy to verify it.

MENSAJE EN CASTELLANO

En primer lugar se agradece feedback para mejorar la estrategia.

Si eres un usuario avanzado y quieres colaborar en mejorar el script no dudes en comentar abajo.

Ten en cuenta que aunque toda esta descripción tenga que estar en inglés no es obligatorio que el comentario esté en inglés.

CHISTE - CASTELLANO

¡Pero Jaime!

¡400.000!

¡Tu da mun!

Range Oscillator Strategy + Stoch Confirm🔹 Short summary

This is a free, educational long-only strategy built on top of the public “Range Oscillator” by Zeiierman (used under CC BY-NC-SA 4.0), combined with a Stochastic timing filter, an EMA-based exit filter and an optional risk-management layer (SL/TP and R-multiple exits). It is NOT financial advice and it is NOT a magic money machine. It’s a structured framework to study how range-expansion + momentum + trend slope can be combined into one rule-based system, often with intentionally RARE trades.

────────────────────────

0. Legal / risk disclaimer

────────────────────────

• This script is FREE and public. I do not charge any fee for it.

• It is for EDUCATIONAL PURPOSES ONLY.

• It is NOT financial advice and does NOT guarantee profits.

• Backtest results can be very different from live results.

• Markets change over time; past performance is NOT indicative of future performance.

• You are fully responsible for your own trades and risk.

Please DO NOT use this script with money you cannot afford to lose. Always start in a demo / paper trading environment and make sure you understand what the logic does before you risk any capital.

────────────────────────

1. About default settings and risk (very important)

────────────────────────

The script is configured with the following defaults in the `strategy()` declaration:

• `initial_capital = 10000`

→ This is only an EXAMPLE account size.

• `default_qty_type = strategy.percent_of_equity`

• `default_qty_value = 100`

→ This means 100% of equity per trade in the default properties.

→ This is AGGRESSIVE and should be treated as a STRESS TEST of the logic, not as a realistic way to trade.

TradingView’s House Rules recommend risking only a small part of equity per trade (often 1–2%, max 5–10% in most cases). To align with these recommendations and to get more realistic backtest results, I STRONGLY RECOMMEND you to:

1. Open **Strategy Settings → Properties**.

2. Set:

• Order size: **Percent of equity**

• Order size (percent): e.g. **1–2%** per trade

3. Make sure **commission** and **slippage** match your own broker conditions.

• By default this script uses `commission_value = 0.1` (0.1%) and `slippage = 3`, which are reasonable example values for many crypto markets.

If you choose to run the strategy with 100% of equity per trade, please treat it ONLY as a stress-test of the logic. It is NOT a sustainable risk model for live trading.

────────────────────────

2. What this strategy tries to do (conceptual overview)

────────────────────────

This is a LONG-ONLY strategy designed to explore the combination of:

1. **Range Oscillator (Zeiierman-based)**

- Measures how far price has moved away from an adaptive mean.

- Uses an ATR-based range to normalize deviation.

- High positive oscillator values indicate strong price expansion away from the mean in a bullish direction.

2. **Stochastic as a timing filter**

- A classic Stochastic (%K and %D) is used.

- The logic requires %K to be below a user-defined level and then crossing above %D.

- This is intended to catch moments when momentum turns up again, rather than chasing every extreme.

3. **EMA Exit Filter (trend slope)**

- An EMA with configurable length (default 70) is calculated.

- The slope of the EMA is monitored: when the slope turns negative while in a long position, and the filter is enabled, it triggers an exit condition.

- This acts as a trend-protection exit: if the medium-term trend starts to weaken, the strategy exits even if the oscillator has not yet fully reverted.

4. **Optional risk-management layer**

- Percentage-based Stop Loss and Take Profit (SL/TP).

- Risk/Reward (R-multiple) exit based on the distance from entry to SL.

- Implemented as OCO orders that work *on top* of the logical exits.

The goal is not to create a “holy grail” system but to serve as a transparent, configurable framework for studying how these concepts behave together on different markets and timeframes.

────────────────────────

3. Components and how they work together

────────────────────────

(1) Range Oscillator (based on “Range Oscillator (Zeiierman)”)

• The script computes a weighted mean price and then measures how far price deviates from that mean.

• Deviation is normalized by an ATR-based range and expressed as an oscillator.

• When the oscillator is above the **entry threshold** (default 100), it signals a strong move away from the mean in the bullish direction.

• When it later drops below the **exit threshold** (default 30), it can trigger an exit (if enabled).

(2) Stochastic confirmation

• Classic Stochastic (%K and %D) is calculated.

• An entry requires:

- %K to be below a user-defined “Cross Level”, and

- then %K to cross above %D.

• This is a momentum confirmation: the strategy tries to enter when momentum turns up from a pullback rather than at any random point.

(3) EMA Exit Filter

• The EMA length is configurable via `emaLength` (default 70).

• The script monitors the EMA slope: it computes the relative change between the current EMA and the previous EMA.

• If the slope turns negative while the strategy holds a long position and the filter is enabled, it triggers an exit condition.

• This is meant to help protect profits or cut losses when the medium-term trend starts to roll over, even if the oscillator conditions are not (yet) signalling exit.

(4) Risk management (optional)

• Stop Loss (SL) and Take Profit (TP):

- Defined as percentages relative to average entry price.

- Both are disabled by default, but you can enable them in the Inputs.

• Risk/Reward Exit:

- Uses the distance from entry to SL to project a profit target at a configurable R-multiple.

- Also optional and disabled by default.

These exits are implemented as `strategy.exit()` OCO orders and can close trades independently of oscillator/EMA conditions if hit first.

────────────────────────

4. Entry & Exit logic (high level)

────────────────────────

A) Time filter

• You can choose a **Start Year** in the Inputs.

• Only candles between the selected start date and 31 Dec 2069 are used for backtesting (`timeCondition`).

• This prevents accidental use of tiny cherry-picked windows and makes tests more honest.

B) Entry condition (long-only)

A long entry is allowed when ALL the following are true:

1. `timeCondition` is true (inside the backtest window).

2. If `useOscEntry` is true:

- Range Oscillator value must be above `entryLevel`.

3. If `useStochEntry` is true:

- Stochastic condition (`stochCondition`) must be true:

- %K < `crossLevel`, then %K crosses above %D.

If these filters agree, the strategy calls `strategy.entry("Long", strategy.long)`.

C) Exit condition (logical exits)

A position can be closed when:

1. `timeCondition` is true AND a long position is open, AND

2. At least one of the following is true:

- If `useOscExit` is true: Oscillator is below `exitLevel`.

- If `useMagicExit` (EMA Exit Filter) is true: EMA slope is negative (`isDown = true`).

In that case, `strategy.close("Long")` is called.

D) Risk-management exits

While a position is open:

• If SL or TP is enabled:

- `strategy.exit("Long Risk", ...)` places an OCO stop/limit order based on the SL/TP percentages.

• If Risk/Reward exit is enabled:

- `strategy.exit("RR Exit", ...)` places an OCO order using a projected R-multiple (`rrMult`) of the SL distance.

These risk-based exits can trigger before the logical oscillator/EMA exits if price hits those levels.

────────────────────────

5. Recommended backtest configuration (to avoid misleading results)

────────────────────────

To align with TradingView House Rules and avoid misleading backtests:

1. **Initial capital**

- 10 000 (or any value you personally want to work with).

2. **Order size**

- Type: **Percent of equity**

- Size: **1–2%** per trade is a reasonable starting point.

- Avoid risking more than 5–10% per trade if you want results that could be sustainable in practice.

3. **Commission & slippage**

- Commission: around 0.1% if that matches your broker.

- Slippage: a few ticks (e.g. 3) to account for real fills.

4. **Timeframe & markets**

- Volatile symbols (e.g. crypto like BTCUSDT, or major indices).

- Timeframes: 1H / 4H / **1D (Daily)** are typical starting points.

- I strongly recommend trying the strategy on **different timeframes**, for example 1D, to see how the behaviour changes between intraday and higher timeframes.

5. **No “caution warning”**

- Make sure your chosen symbol + timeframe + settings do not trigger TradingView’s caution messages.

- If you see warnings (e.g. “too few trades”), adjust timeframe/symbol or the backtest period.

────────────────────────

5a. About low trade count and rare signals

────────────────────────

This strategy is intentionally designed to trade RARELY:

• It is **long-only**.

• It uses strict filters (Range Oscillator threshold + Stochastic confirmation + optional EMA Exit Filter).

• On higher timeframes (especially **1D / Daily**) this can result in a **low total number of trades**, sometimes WELL BELOW 100 trades over the whole backtest.

TradingView’s House Rules mention 100+ trades as a guideline for more robust statistics. In this specific case:

• The **low trade count is a conscious design choice**, not an attempt to cherry-pick a tiny, ultra-profitable window.

• The goal is to study a **small number of high-conviction long entries** on higher timeframes, not to generate frequent intraday signals.

• Because of the low trade count, results should NOT be interpreted as statistically strong or “proven” – they are only one sample of how this logic would have behaved on past data.

Please keep this in mind when you look at the equity curve and performance metrics. A beautiful curve with only a handful of trades is still just a small sample.

────────────────────────

6. How to use this strategy (step-by-step)

────────────────────────

1. Add the script to your chart.

2. Open the **Inputs** tab:

- Set the backtest start year.

- Decide whether to use Oscillator-based entry/exit, Stochastic confirmation, and EMA Exit Filter.

- Optionally enable SL, TP, and Risk/Reward exits.

3. Open the **Properties** tab:

- Set a realistic account size if you want.

- Set order size to a realistic % of equity (e.g. 1–2%).

- Confirm that commission and slippage are realistic for your broker.

4. Run the backtest:

- Look at Net Profit, Max Drawdown, number of trades, and equity curve.

- Remember that a low trade count means the statistics are not very strong.

5. Experiment:

- Tweak thresholds (`entryLevel`, `exitLevel`), Stochastic settings, EMA length, and risk params.

- See how the metrics and trade frequency change.

6. Forward-test:

- Before using any idea in live trading, forward-test on a demo account and observe behaviour in real time.

────────────────────────

7. Originality and usefulness (why this is more than a mashup)

────────────────────────

This script is not intended to be a random visual mashup of indicators. It is designed as a coherent, testable strategy with clear roles for each component:

• Range Oscillator:

- Handles mean vs. range-expansion states via an adaptive, ATR-normalized metric.

• Stochastic:

- Acts as a timing filter to avoid entering purely on extremes and instead waits for momentum to turn.

• EMA Exit Filter:

- Trend-slope-based safety net to exit when the medium-term direction changes against the position.

• Risk module:

- Provides practical, rule-based exits: SL, TP, and R-multiple exit, which are useful for structuring risk even if you modify the core logic.

It aims to give traders a ready-made **framework to study and modify**, not a black box or “signals” product.

────────────────────────

8. Limitations and good practices

────────────────────────

• No single strategy works on all markets or in all regimes.

• This script is long-only; it does not short the market.

• Performance can degrade when market structure changes.

• Overfitting (curve fitting) is a real risk if you endlessly tweak parameters to maximise historical profit.

Good practices:

- Test on multiple symbols and timeframes.

- Focus on stability and drawdown, not only on how high the profit line goes.

- View this as a learning tool and a basis for your own research.

────────────────────────

9. Licensing and credits

────────────────────────

• Core oscillator idea & base code:

- “Range Oscillator (Zeiierman)”

- © Zeiierman, licensed under CC BY-NC-SA 4.0.

• Strategy logic, Stochastic confirmation, EMA Exit Filter, and risk-management layer:

- Modifications by jokiniemi.

Please respect both the original license and TradingView House Rules if you fork or republish any part of this script.

────────────────────────

10. No payments / no vendor pitch

────────────────────────

• This script is completely FREE to use on TradingView.

• There is no paid subscription, no external payment link, and no private signals group attached to it.

• If you have questions, please use TradingView’s comment system or private messages instead of expecting financial advice.

Use this script as a tool to learn, experiment, and build your own understanding of markets.

────────────────────────

11. Example backtest settings used in screenshots

────────────────────────

To avoid any confusion about how the results shown in screenshots were produced, here is one concrete example configuration:

• Symbol: BTCUSDT (or similar major BTC pair)

• Timeframe: 1D (Daily)

• Backtest period: from 2018 to the most recent data

• Initial capital: 10 000

• Order size type: Percent of equity

• Order size: 2% per trade

• Commission: 0.1%

• Slippage: 3 ticks

• Risk settings: Stop Loss and Take Profit disabled by default, Risk/Reward exit disabled by default

• Filters: Range Oscillator entry/exit enabled, Stochastic confirmation enabled, EMA Exit Filter enabled

If you change any of these settings (symbol, timeframe, risk per trade, commission, slippage, filters, etc.), your results will look different. Please always adapt the configuration to your own risk tolerance, market, and trading style.

JMA Quantum Edge: Adaptive Precision Trading System JMA Quantum Edge: Adaptive Precision Trading System - Enhanced Visuals & Risk Management

Get ready to experience a groundbreaking trading strategy that adapts in real-time to market conditions! This powerful, open-source script combines advanced technical analysis with state-of-the-art risk management tools, designed to give you the edge you need in today's dynamic markets.

What It Does:

Adaptive JMA Indicator:

Utilizes a custom Jurik Moving Average (JMA) that adjusts its sensitivity based on market volatility, ensuring you get precise signals even in the most fluctuating environments.

Dynamic Risk Management:

Features built-in support for partial exits (scaling out) to secure profits, along with an optional Kelly Criterion-based position sizing that tailors your exposure based on historical performance metrics.

Robust Error Handling:

Incorporates market condition filters—like minimum volume and maximum allowed gap percentage—to ensure trades are only executed under favorable conditions.

Vivid Visual Enhancements:

Enjoy an animated background that reflects market momentum, dynamic pivot markers, and clearly drawn trend channels. Plus, interactive tables provide real-time performance analytics and detailed error metrics.

Fully Customizable:

With a comprehensive set of inputs, you can easily tailor the strategy to your personal trading style and market preferences. Adjust everything from JMA parameters to refresh intervals for tables and labels!

How to Use It:

Add the Script:

Copy and paste the script into the Pine Script Editor on TradingView and click “Add to Chart.”

Configure Your Settings:

Customize your risk management (capital, commission, position sizing, partial exits, etc.) and tweak the JMA settings to match your preferred trading style. Use the extensive input panel to adjust visuals, alerts, and more.

Backtest & Optimize:

Run the strategy in the Strategy Tester to analyze its historical performance. Monitor real-time analytics and error metrics via the interactive tables, and fine-tune your parameters for optimal performance.

Go Live with Confidence:

Once you're satisfied with the backtest results, use the generated signals for live trading, and let the system help you stay ahead in fast-paced markets!

How to use the imputs:

This cutting-edge strategy is designed to adapt to changing market conditions and offers you complete control over your trading parameters. Here’s a breakdown of what each group of inputs does and how you should use them:

Risk Management & Trade Settings

Recalculate on Every Tick:

What it does: When enabled, the strategy recalculates on every price update.

Recommendation: Leave it true for fast charts.

Initial Capital:

What it does: Sets your starting capital for backtesting, which influences position sizing and performance metrics.

Recommendation: Start with $10,000 (or adjust according to your trading capital).

Commission (%):

What it does: Simulates the cost per trade.

Recommendation: Use a realistic rate (e.g., 0.04%).

Position Size & Quantity Type:

What they do: Define how large each trade will be. Choose between a fixed unit amount or a percentage of equity.

Recommendation: For beginners, the default fixed value is a good start. Experiment later with percentage-based sizing if needed.

Order Comment:

What it does: Adds a label to your orders for easier tracking.

Allow Reverse Orders:

What it does: If disabled, the strategy will close opposing positions before entering a new trade, reducing conflicts.

Enable Dynamic Position Sizing:

What it does: Adjusts trade size based on current volatility.

Recommendation: Beginners may start with this disabled until they understand basic sizing.

Partial Exit Inputs:

What they do:

Enable Partial Exits: When turned on, you can scale out of your position to lock in profits.

Partial Exit Profit (%): The profit percentage that triggers a partial exit.

Partial Exit Percentage: The percentage of your current position to exit. Recommendation: Use defaults (e.g., 5% profit, 50% exit) to secure profits gradually.

Kelly Criterion Option:

What it does: When enabled, adjusts your position sizing using historical performance (win rate and profit factor).

Recommendation: Beginners might leave this disabled until comfortable with backtest performance metrics.

Market Condition Filters:

What they do:

Minimum Volume: Ensures trades occur only when there’s sufficient market activity.

Maximum Gap (%): Prevents trading if there’s an unusually large gap between the previous close and current open. Recommendation: Defaults work well for most markets. If trades seem erratic, consider tightening these limits.

JMA Settings

Price Source:

What it does: The input series for the JMA calculation, typically set to the closing price.

JMA Length:

What it does: Controls the smoothing period of the JMA. Lower values are more sensitive; higher values smooth out the noise. Recommendation: Start with 21.

JMA Phase & Power:

What they do: Adjust how responsive the JMA is. Phase controls timing; power adjusts the intensity. Recommendation: Default settings (63 phase and 3 power) are a balanced starting point.

Visual Settings & Style

Show JMA Line, Pivot Lines, and Pivot Labels:

What they do: Toggle visual elements on your chart for easier signal identification.

Pivot History Count:

What it does: Limits how many historical pivot markers are displayed.

Color Settings (Up/Down Neon Colors):

What they do: Set the visual cues for buy and sell signals.

Pivot Marker & Line Style:

What they do: Choose the style and thickness of your pivot markers and lines.

Show Stats Panel:

What it does: Displays real-time performance and error metrics.

Dynamic Background & Visual Enhancements

Animate Background:

What it does: Changes the background color based on market momentum.

Show Trend Channels & Volume Zones:

What they do: Draw trend channels and highlight areas of high volatility/volume.

Show Data-Rich Labels:

What it does: Displays key metrics like volume, error percentage, and momentum on the chart.

High Volatility Threshold:

What it does: Determines the multiplier for when the chart background should change due to high volatility.

Multi-Timeframe Settings

Higher Timeframe:

What it does: Uses a higher timeframe’s JMA for trend confirmation. Recommendation: Use Daily ('D') or Weekly ('W') for broader trend analysis.

Show HTF Trend Zone & Opacity:

What they do: Display a visual zone from the higher timeframe to help confirm trends.

6. Trailing Stop Settings

Trailing Stop ATR Factor & Offset Multiplier:

What they do: Calculate trailing stops based on the Average True Range (ATR), adjusting stop distances dynamically. Recommendation: Default settings are a good balance but can be fine-tuned based on asset volatility.

Alerts & Notifications

Alerts on Pivot Formation & JMA Crossover:

What they do: Notify you when key events occur.

Dynamic Power Threshold:

What it does: Sets the sensitivity for dynamic alerts.

8. Static Stop Loss / Take Profit

Static Stop Loss (%) & Take Profit (%):

What they do: Allow you to set fixed stop loss or take profit levels. Recommendation: Leave them at 0 to disable if you prefer dynamic risk management, or set them if you have strict risk/reward preferences.

Advanced Settings

ATR Length:

What it does: Determines the period for ATR calculation, impacting trailing stop sensitivity. Recommendation: Start with 14.

Optimization Feedback & Enhanced Error Analysis

Error Metric Length & Error Threshold (%):

What they do: Calculate error metrics (like average error, skewness, and kurtosis) to help you fine-tune the JMA. Recommendation: Use the defaults and adjust if the error metrics seem off during backtesting.

UI - User-Driven Tweaking & Table Customization

Parameter Tweaker Panel, Debug/Performance Table Settings:

What they do: Provide interactive tables that display real-time performance, error metrics, and allow you to monitor strategy parameters.

Refresh Frequency Options (Table & Label Refresh Intervals):

What they do: Set how often the tables and labels update.

Recommendation: Start with an interval of 1 bar; increase it if your chart is too busy.

Important for Beginners:

Default Settings:

All default values have been chosen for balanced performance across different markets. If you ever experience unexpected behavior, start by resetting the inputs to their defaults.

Step-by-Step Adjustments:

Experiment by changing one setting at a time while observing how the strategy’s signals and performance metrics change. This will help you understand the impact of each parameter.

Resetting to Defaults:

If things seem off or you’re not getting the expected results, you can always reset the indicator. Either reload the script or use the “Reset Inputs” option (if available) to revert to the default settings.

Jump in, experiment, and enjoy the power of adaptive precision trading. This strategy is built to grow with your skills—have fun exploring and refining your trading edge!

Happy trading!

HOD/LOD/PMH/PML/PDH/PDL Strategy by @tradingbauhaus This script is a trading strategy @tradingbauhaus designed to trade based on key price levels, such as the High of Day (HOD), Low of Day (LOD), Premarket High (PMH), Premarket Low (PML), Previous Day High (PDH), and Previous Day Low (PDL). Below, I’ll explain in detail what the script does:

Core Functionality of the Script:

Calculates Key Price Levels:

HOD (High of Day): The highest price of the current day.

LOD (Low of Day): The lowest price of the current day.

PMH (Premarket High): The highest price during the premarket session (before the market opens).

PML (Premarket Low): The lowest price during the premarket session.

PDH (Previous Day High): The highest price of the previous day.

PDL (Previous Day Low): The lowest price of the previous day.

Draws Horizontal Lines on the Chart:

Plots horizontal lines on the chart for each key level (HOD, LOD, PMH, PML, PDH, PDL) with specific colors for easy visual identification.

Defines Entry and Exit Rules:

Long Entry (Buy): If the price crosses above the PMH (Premarket High) or the PDH (Previous Day High).

Short Entry (Sell): If the price crosses below the PML (Premarket Low) or the PDL (Previous Day Low).

Long Exit: If the price reaches the HOD (High of Day) during a long position.

Short Exit: If the price reaches the LOD (Low of Day) during a short position.

How the Script Works Step by Step:

Calculates Key Levels:

Uses the request.security function to fetch the HOD and LOD of the current day, as well as the highs and lows of the previous day (PDH and PDL).

Calculates the PMH and PML during the premarket session (before 9:30 AM).

Plots Levels on the Chart:

Uses the plot function to draw horizontal lines on the chart representing the key levels (HOD, LOD, PMH, PML, PDH, PDL).

Each level has a specific color for easy identification:

HOD: White.

LOD: Purple.

PDH: Orange.

PDL: Blue.

PMH: Green.

PML: Red.

Defines Trading Rules:

Uses conditions with ta.crossover and ta.crossunder to detect when the price crosses key levels.

Long Entry: If the price crosses above the PMH or PDH, a long position (buy) is opened.

Short Entry: If the price crosses below the PML or PDL, a short position (sell) is opened.

Long Exit: If the price reaches the HOD during a long position, the position is closed.

Short Exit: If the price reaches the LOD during a short position, the position is closed.

Executes Orders Automatically:

Uses the strategy.entry and strategy.close functions to open and close positions automatically based on the defined rules.

Advantages of This Strategy:

Based on Key Levels: Uses important price levels that often act as support and resistance.

Easy to Visualize: Horizontal lines on the chart make it easy to identify levels.

Automated: Entries and exits are executed automatically based on the defined rules.

Limitations of This Strategy:

Dependent on Volatility: Works best in markets with significant price movements.

False Crosses: There may be false crosses that generate incorrect signals.

No Advanced Risk Management: Does not include dynamic stop-loss or take-profit mechanisms.

How to Improve the Strategy:

Add Stop-Loss and Take-Profit: To limit losses and lock in profits.

Filter Signals with Indicators: Use RSI, MACD, or other indicators to confirm signals.

Optimize Levels: Adjust key levels based on the asset’s behavior.

In summary, this script is a trading strategy that operates based on key price levels, such as HOD, LOD, PMH, PML, PDH, and PDL. It is useful for traders who want to trade based on significant support and resistance levels.

Dual Strategy Selector V2 - CryptogyaniOverview:

This script provides traders with a dual-strategy system that they can toggle between using a simple dropdown menu in the input settings. It is designed to cater to different trading styles and needs, offering both simplicity and advanced filtering techniques. The strategies are built around moving average crossovers, enhanced by configurable risk management tools like take profit levels, trailing stops, and ATR-based stop-loss.

Key Features:

Two Strategies in One Script:

Strategy 1: A classic moving average crossover strategy for identifying entry signals based on trend reversals. Includes user-defined take profit and trailing stop-loss options for profit locking.

Strategy 2: An advanced trend-following system that incorporates:

A higher timeframe trend filter to confirm entry signals.

ATR-based stop-loss for dynamic risk management.

Configurable partial take profit to secure gains while letting the trade run.

Highly Customizable:

All key parameters such as SMA lengths, take profit levels, ATR multiplier, and timeframe for the trend filter are adjustable via the input settings.

Dynamic Toggle:

Traders can switch between Strategy 1 and Strategy 2 with a single dropdown, allowing them to adapt the strategy to market conditions.

How It Works:

Strategy 1:

Entry Logic: A long trade is triggered when the fast SMA crosses above the slow SMA.

Exit Logic: The trade exits at either a user-defined take profit level (percentage or pips) or via an optional trailing stop that dynamically adjusts based on price movement.

Strategy 2:

Entry Logic: Builds on the SMA crossover logic but adds a higher timeframe trend filter to align trades with the broader market direction.

Risk Management:

ATR-Based Stop-Loss: Protects against adverse moves with a volatility-adjusted stop-loss.

Partial Take Profit: Allows traders to secure a percentage of gains while keeping some exposure for extended trends.

How to Use:

Select Your Strategy:

Use the dropdown in the input settings to choose Strategy 1 or Strategy 2.

Configure Parameters:

Adjust SMA lengths, take profit, and risk management settings to align with your trading style.

For Strategy 2, specify the higher timeframe for trend filtering.

Deploy and Monitor:

Apply the script to your preferred asset and timeframe.

Use the backtest results to fine-tune settings for optimal performance.

Why Choose This Script?:

This script stands out due to its dual-strategy flexibility and enhanced features:

For beginners: Strategy 1 provides a simple yet effective trend-following system with minimal setup.

For advanced traders: Strategy 2 includes powerful tools like trend filters and ATR-based stop-loss, making it ideal for challenging market conditions.

By combining simplicity with advanced features, this script offers something for everyone while maintaining full transparency and user customization.

Default Settings:

Strategy 1:

Fast SMA: 21, Slow SMA: 49

Take Profit: 7% or 50 pips

Trailing Stop: Optional (disabled by default)

Strategy 2:

Fast SMA: 20, Slow SMA: 50

ATR Multiplier: 1.5

Partial Take Profit: 50%

Higher Timeframe: 1 Day (1D)